FILE REVISED INCOME TAX RETURN FOR FINANCIAL YEAR - 2022-23, In The Following Cases :

- By Team of D. Saha & Co.

Revised Income Tax Returns for the Assessment Year 2023-24 can be filed till 31 December 2023. The revision can be done even after the return has been processed by the tax department. If you made a mistake in your tax return, you can rectify it by filing a revised return. Find out why, when and how to do it.Case 1 : Shivangi Saha, Kolkata-based graphic designer’s monthly income had increased 40% to nearly Rs.75,000, yet the tax remained zero. Her new employer neither deducted any tax nor asked her to show tax-saving investments proof. The good times didn’t last, though. Saha’s delight changed to dismay when she sat down to file her tax return last month. Her new employer had missed her previous job income and, therefore, did not deduct any tax. With no tax saving investments to show, except the mandatory Provident Fund contribution, she was saddled with a heavy tax liability.

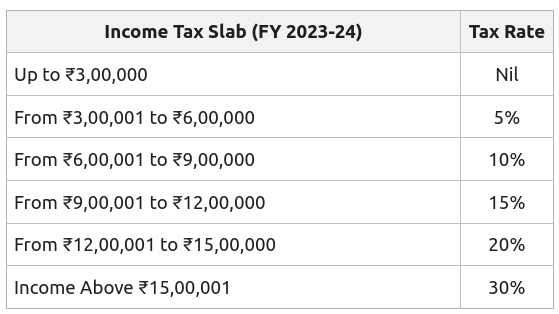

There is a sliver of hope for taxpayers like Saha. Under Section 139(5) of the Income Tax Act 1961, she can file a revised tax return and opt for the new tax regime. Revised returns for the current assessment year can be filed till 31 December 2023. The revision can be done even after the return has been processed by the tax department. Under the new tax regime for the financial year 2022-23, Saha will not get the benefit of Rs.50,000 standard deduction or her contribution to the Provident Fund, but her tax would be lesser due to the lower tax rates resulting to savings of about Rs.3,200 tax under the new regime.

Case 2 : Pune-based Software Engineer Surajit Bose, who filed his ITR in July, have duly included the income from interest and dividends as per Form 26AS, but did not mention the capital gains of Rs.2.25 lakh from stocks and equity funds reflected in Annual Information Statement (AIS), which he subsequently noticed.

Bose can expect a notice with penalty from the tax department for the omission when his return is processed. The department has information on all financial transactions conducted by the individual during the year. Banks and NBFCs report all interest paid on deposits and savings accounts, brokerages and mutual funds report capital gains and dividends, credit card issuers report high-value transactions, tenants report payment of rent and forex dealers report purchase of foreign currency. This puts taxpayers like Bose on a sticky wicket. This is why it is recommended that taxpayers should reconcile the information in the AIS while filing their tax returns.

At the same time, taxpayers should not blindly follow the AIS. It takes time for details to get updated in the AIS. Even then, some types of income may not get captured in the form. For instance, the interest on small savings schemes won’t be mentioned in the AIS. Revised returns can be filed even by taxpayers who filed belated returns after the 31 July dead line. Also, there is no limit to the number of revised returns that one can file. This is not recommended though. Too many revisions can invite a closer scrutiny by the tax authorities.

Case 3 : Chennai-based IT professional Mehuli Sarkar filed her return in July, but is contemplating revising it. According to her the HRA component in her Form 16 is very low and she wants to increase the HRA component to claim a higher exemption which could fetch a tax refund.

What she doesn’t realize is that instead of a tax refund, she might get a tax notice. One should avoid misusing the facility to file a revised return. Too many revisions can invite a closer scrutiny by the tax authorities. The Form 16 is a legal document and the HRA component mentioned in it cannot be changed at will. The tax department already has the Form 16 filed by Sarkar’s employer. If she files a revised return and claims a higher HRA exemption, the mismatch will immediately be detected by the tax department. The revised return will most probably get rejected and she might even have to explain why she is claiming more than the HRA received from her employer.

Case 4 : Subhankar Bhattacharjee, Bangalore-based GST practitioner left his regular job last year and became a consultant in his company. Under the new arrangement, he gets a lump-sum amount with a 10% TDS. He claims deduction for some expenses, such as travel, rent and purchase of accessories, but even then his tax outgo is quite high. He can reduce his tax significantly by opting for presumptive taxation. Under this, 50% of income from businesses or specified professions is presumed to be deductions.

If you, too, have made a mistake in your tax return, you can file a revised ITR. The mistake can be as simple as choosing the wrong tax regime or listing incorrect bank account details. There can also be serious mistakes that could lead to a tax notice and stiff penalties.

Besides revising their tax returns, taxpayers can now also update their previous returns. The concept of updated tax returns was introduced last year. Eligible taxpayers can update their ITRs by paying additional tax, interest or penalty. This was done to increase voluntary compliance and avoid penalties if an omission was detected by the tax authorities. Updated Returns can be filed within 24 months from the end of the relevant Assessment Year. However, this is allowed only if it results in additional payment of tax. An Updated Return cannot be filed to claim a tax refund. Taxpayers have also become jittery after reading media reports about tax notices to those who furnished incorrect information in their returns, or claimed false deductions or exemptions. The penalty is 25% of the additional tax due for up to one year’s delay, and 50% after one year and before two years. Think of this as an amnesty scheme by the tax department. This way you can avoid higher penalties and interest if the discrepancies are later discovered.

Last Date of Income Tax Revised Return Filing is 31/12/2023 or before the Assessment is made, whichever is earlier.Disclaimer :- (You are advised to consult your Legal Counsel before taking any decisions. This is issued only for the purpose of public awareness and information. The Contributor or any of his employees/associates will not take any responsibility for any actions of the reader based directly or indirectly on the basis of the above Article.)

Please share your valuable suggestions/opinions/feedback.

Our e-mail id : info@kolkatataxconsultants.in

Contact nos. : 8420159817 / 9674797985

- CARL SANDBURG (American Poet & Journalist)

- CARL SANDBURG (American Poet & Journalist)